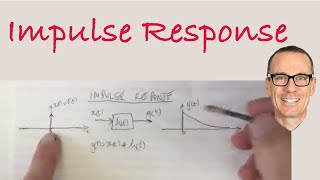

Media Summary: Asset Pricing with Prof. John H. Cochrane PART II. Module 3. Time Series Predictability, Volatility, and Bubbles More course ... This lecture tests the RBC model using a structural VAR model, and compares the Demonstration of the new *lpirf* command in Stata 18 for local-projection estimates of

Impulse Response Functions - Detailed Analysis & Overview

Asset Pricing with Prof. John H. Cochrane PART II. Module 3. Time Series Predictability, Volatility, and Bubbles More course ... This lecture tests the RBC model using a structural VAR model, and compares the Demonstration of the new *lpirf* command in Stata 18 for local-projection estimates of In this video, we'll take a step back and look at the I was recently looking for a video explaining MIT RES.18-009 Learn Differential Equations: Up Close with Gilbert Strang and Cleve Moler, Fall 2015 View the complete course: ...

I welcome to Imperium loading the topic of this video is going to be Okay so in this video i will discuss how to design