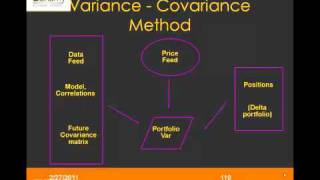

Media Summary: Stability Studies in Pharma ICH Guidelines Explained ( Every major bank, hedge fund, and DeFi protocol needs to answer one question: how much could we lose on a really bad day? Stata has two commands for estimating a reduced-form VARs:

Var Q1a - Detailed Analysis & Overview

Stability Studies in Pharma ICH Guidelines Explained ( Every major bank, hedge fund, and DeFi protocol needs to answer one question: how much could we lose on a really bad day? Stata has two commands for estimating a reduced-form VARs: ICH QA R2 STABILITY TESTING OF NEW DRUG SUBSTANCES AND PRODUCTS. What happens when a financial model updates its definition of a worst-case scenario? We dive deep into the evolution of modern ... Dive into the world of financial risk management with this comprehensive guide to

This is Lecture 5 in my Econometrics course at Swansea University. Watch Live on The Economic Society Facebook page Every ... KV3: Recursive Forecasting of VAR(1). How to use a VAR(1) model for computing forecasts efficiently In Part 2b, we continue with our discussion of